Built-for-Purpose

Compliance Technology.

Alongside our advisory practice, we build practical compliance tools that put expert-grade AML/CTF capability directly in your hands.

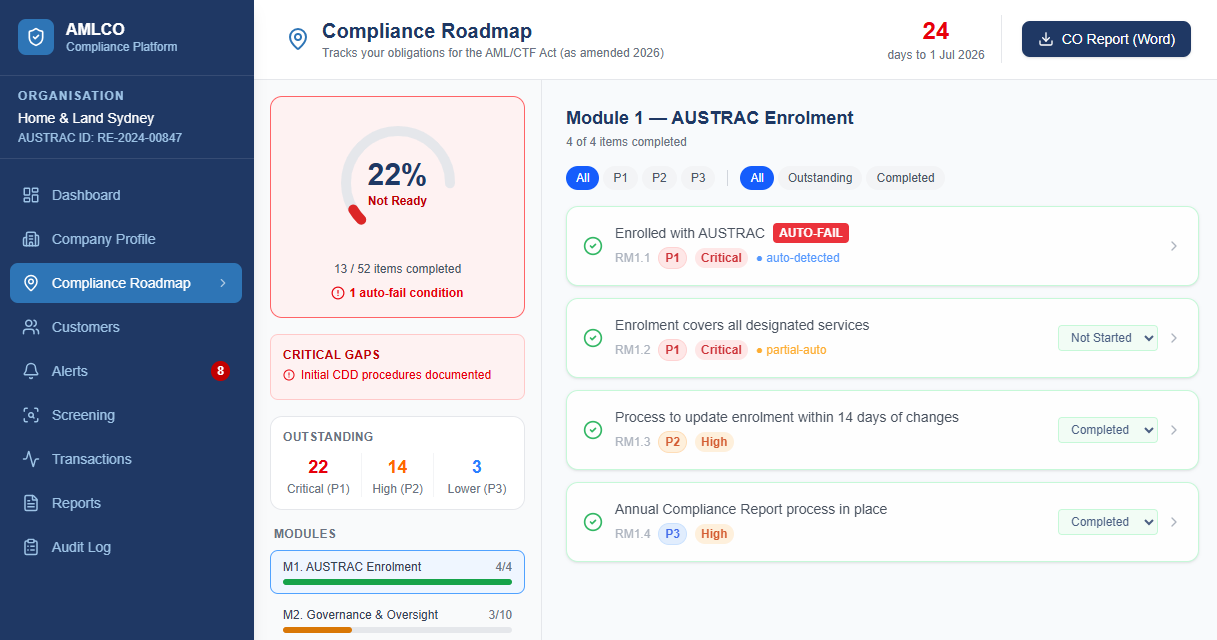

Know exactly where you stand before 1 July 2026. Enter your business details and instantly get a personalised compliance readiness score (0–100%), a 52-item obligations roadmap showing what to fix in priority order, and a downloadable CO Report — completely free.

Compliance Platform

Stop piecing together compliance from scratch. Our AI-powered platform generates a complete, AUSTRAC-aligned AML/CTF program tailored to your business — in minutes, not months. Built by compliance specialists. Designed for reporting entities who need it done right, fast.

Screen individuals and entities against global sanctions lists in seconds. SanctionCheck delivers fast, reliable results against OFAC, UN, DFAT, and other major sanctions regimes — giving your team the confidence to onboard customers and process transactions without compliance blind spots.

Run a Sanctions CheckPolicy Document

Need a compliant AML/CTF policy document today? RapidAML delivers a professionally drafted, AUSTRAC-aligned policy template for just A$49 — available instantly. The most affordable way for Tranche 2 entities to get a solid compliance foundation in place before the deadline.

Get RapidAML — A$49